The comprehensive health care reform law enacted in March 2010 (sometimes known as ACA, PPACA, or “Obamacare”).

The law has 3 primary goals:

Make affordable health insurance available to more people. The law provides consumers with subsidies (“premium tax credits”) that lower costs for households with incomes between 100% and 400% of the federal poverty level.

Expand the Medicaid program to cover all adults with income below 138% of the federal poverty level. (Not all states have expanded their Medicaid programs.)

Support innovative medical care delivery methods designed to lower the costs of health care generally.

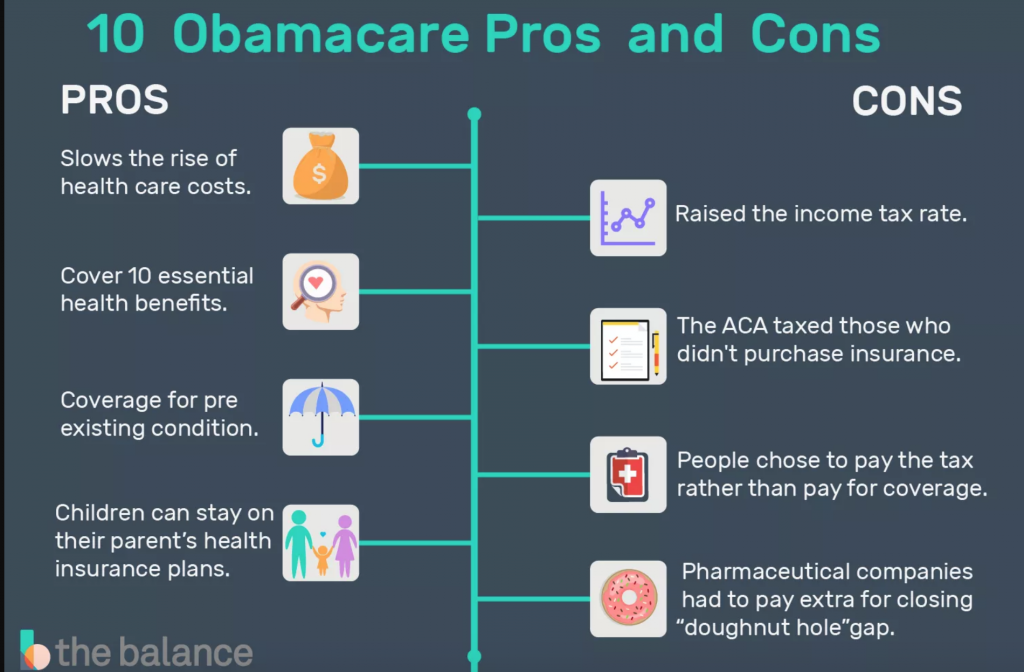

The biggest benefit of the ACA is that it slows the rise of health care costs. It does this by providing insurance for millions and making preventive care free. This means people receive treatment before they need expensive emergency room services. In 2016, the cost of health care services increased 1.2 percent for the year. That’s much less than the price increase of 4 percent in 2004.

It requires all insurance plans to cover 10 essential health benefits. These include treatment for mental health, addiction, and chronic diseases. Without these services, many patients wind up in the emergency room. Those costs are passed onto Medicaid and therefore the taxpayer.

It eliminates lifetime and annual coverage limits. Insurance companies used this to contain costs to $1 million per year. Beneficiaries who exceeded that limit had to pay 100 percent of costs.

Children can stay on their parents’ health insurance plans up to age 26. As of 2012, more than 3 million previously uninsured young people were added. This increased profit for insurance companies. They receive more premiums from these healthy individuals.

States must set up insurance exchanges or use the federal government’s exchange. Either method makes it easier to shop for plans.

The middle class (earning up to 400 percent of the poverty level) receive tax credits on their premiums. It expands Medicaid to 138 percent of the federal poverty level. It provides this coverage to adults without children for the first time.

It eliminates the Medicare “doughnut hole” gap in coverage by 2020.

Businesses with more than 50 employees must offer health insurance. They receive tax credits to help with the costs.

It lowers the budget deficit by $143 billion by 2022 according to the Congressional Budget Office. It does this in three ways. First, it reduces the government’s health care costs. Second, it raises taxes on some businesses and higher income families. Third, it shifts cost burdens to health care providers and pharmacy companies.

Cons

Three million to 5 million people lost their employment-based health insurance. Many businesses found it more cost-effective to pay the penalty and let their employees purchase insurance plans on the exchanges. Other small businesses find they can get better plans through the state-run exchanges.

Thirty million people never had company plans and relied on private health insurance. Insurance companies canceled many of their plans because their policies didn’t cover the ACA’s 10 essential benefits. For those who lost those cut-rate plans, the costs of replacing them are high. The ACA requires services that many people don’t need, like maternity care.

Increased coverage raised overall health care costs in the short term. That’s because many people received preventive care and testing for the first time. It was expensive to treat illnesses that had been ignored for decades.

The ACA taxed those who didn’t purchase insurance. But many avoided the tax through an ever-expanding list of exemptions.

In 2013, the ACA raised the income tax rate for 1 million individuals with incomes above $200,000. It also raised taxes for 4 million couples filing joint returns on incomes exceeding $250,000. The rate increased from 1.45 percent to 2.35 percent on income above the threshold. They also pay an additional 3.8 percent Medicare tax. That applies to the lesser of income from dividends, capital gains, rent and royalties or income above the threshold.

Starting in 2013, medical device manufacturers and importers paid a 2.3 percent excise tax. Note: This tax was suspended for 2016-2018. Indoor tanning services paid a 10 percent excise tax. This might discourage those businesses from hiring new employees.

Starting in 2013, families can deduct medical expenses that exceed 10 percent of income. Before, they could deduct any expenses that exceeded 7.5 percent of income.

Pharmaceutical companies pay an extra $84.8 billion in fees between 2013 and 2023. That pays for closing the “doughnut hole” in Medicare Part D. Drug costs could rise if the companies pass this onto consumers.